The alternative data industry is still showing considerable growth. Over the past few years, alternative data is no longer a unique edge, it’s table stakes.

Our “Alternative Data Buy-side Insights & Trends 2026” report, recently featured in Hedgeweek, reflects the industry’s momentum, specifically around how internal resources dedicated to alternative data are changing, including budget allocation, staffing, technology investment, and senior leadership commitment. The results show a clear pattern, that firms are professionalising their alternative data efforts, with technology at the core.

In the first blog of our series surrounding our latest report, we’ll be unpacking the insights and what this means for the future of alt data.

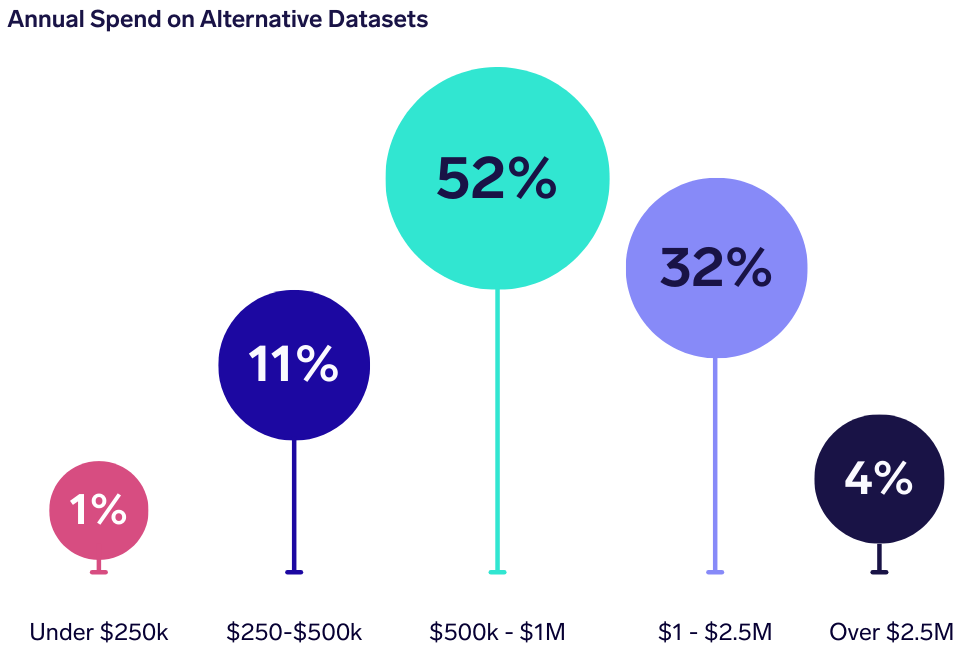

How Much are Firms Investing Today?

Our research shows that alternative data budgets are concentrated firmly in the mid-range:

- 52% of firms spend $500k–$1M annually

- 32% allocate $1M–$2.5M

- 11% spend $250k–$500k

- 1% spend $250k or less

- 4% spend more than $2.5M

In total, over 80% of respondents are investing between $500k and $2.5M per year.

This suggests meaningful commitment, alternative data is clearly embedded in research budgets, but spending remains disciplined. Most firms are not overspending indiscriminately and are focused on investing at levels that support structured deployment and measurable ROI.

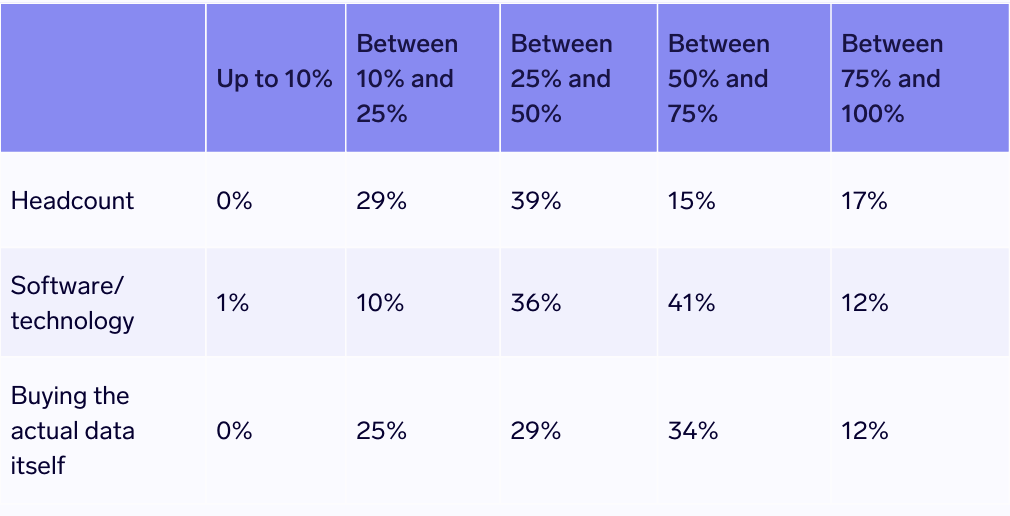

Technology Takes the Lion’s Share of Budget

When examining how firms allocate their alternative data budgets, a clear hierarchy emerges.

- Headcount typically accounts for 10-50% of budget allocation. Personnel remains critical, but it is not the largest cost centre.

- Software and technology see heavier investment, with most firms allocating 25-75% of their budgets to tools that analyse, manage, and operationalise data.

- Data acquisition itself also sits in the 25-75% range, suggesting a balanced approach between purchasing datasets and enabling them through infrastructure and talent.

The message is clear, alternative data success is no longer about simply buying datasets. Funds are prioritising the platforms, workflows, and analytical tools required to extract value from them.

This shift reflects a maturing market. Competitive advantage increasingly comes from integration, automation, and speed of insight, not from raw data access alone.

Dedicated Leads are Now Universal & Senior Management Commitment is Strong

One of the key findings showed that 100% of respondents report having a dedicated alternative data lead. This represents a 16% increase from our 2025 survey, where 11% of firms indicated they did not have a dedicated lead.

Alternative data has moved from a decentralised, ad hoc initiative to a formally owned function. Dedicated leadership brings:

- Centralised vendor management

- Governance and compliance oversight

- Budget accountability

- Strategic alignment with portfolio managers

This institutionalisation signals that alternative data is no longer optional, it is embedded within research infrastructure.

Leadership commitment mirrors this structural shift.

- 58% of respondents describe senior management as “quite committed”

- 42% describe them as “very committed”

Notably, there were no indications of weak or passive executive support. This level of top-down endorsement is critical. Without senior buy-in, alternative data initiatives often stall at pilot stage. Instead, we are seeing sustained investment, clear ownership, and organisational alignment.

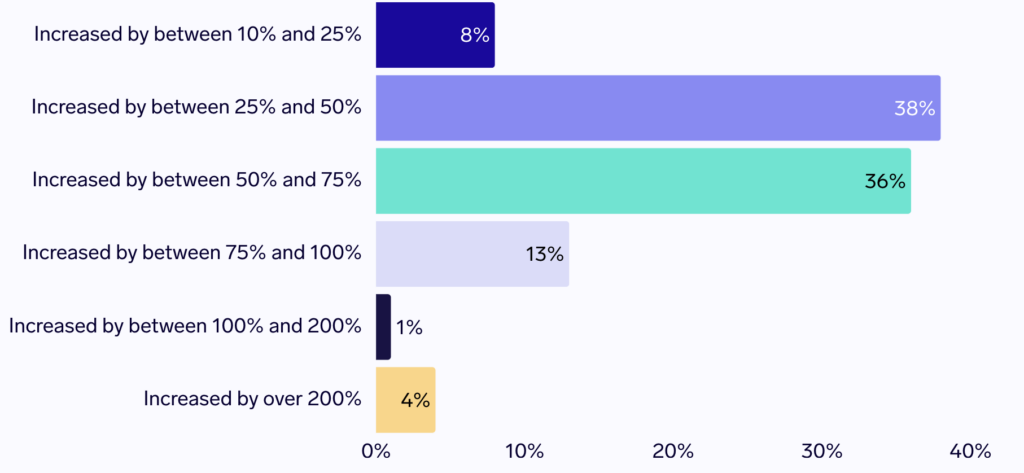

Budgets are Growing, and Growing Fast

Investment in alternative data is not just stable, it is accelerating. Compared to two years ago:

- 38% of firms report budget increases of 25–50%

- 36% report growth of 50–75%

- 4% report increases of over 200%

This is not incremental inflation. It reflects structural scaling. Firms are expanding dataset coverage, upgrading tooling, and adding specialist resources. As strategies become more data-intensive, the supporting infrastructure must scale accordingly.

2026 Reflects Continued Expansion

Looking forward, respondents expect further budget growth in 2026:

- 76% anticipate budgets will increase modestly

- 18% expect a substantial increase

- Only 6% expect budgets to remain the same

Importantly, none expect contraction. This signals confidence. Alternative data is viewed not as experimental, but as a durable and expanding component of alpha generation.

The Bigger Picture: From Adoption to Optimization

Taken together, these findings mark a shift from adoption to optimization. Our report showed that:

- Formal leadership structures

- Strong executive sponsorship

- Technology-first budget allocation

- Sustained and accelerating investment

The next phase of competitive differentiation will not simply be about who uses alternative data, but who integrates it most effectively.

As budgets rise and infrastructure matures, the focus will increasingly move toward workflow efficiency, cross-team collaboration, and extracting scalable insight from ever-expanding datasets.

Download the Full Report

This is just one section of our latest research into how portfolio managers and analysts are approaching alternative data in 2026.

To explore the full findings, including budget benchmarks, adoption trends, use cases, and future outlook, download the complete report here and see how your firm compares to peers across the industry.